Write your awesome label here.

Capital game

Insured vs. Conventional Mortgages: What You Need to Know Before Buying a Home

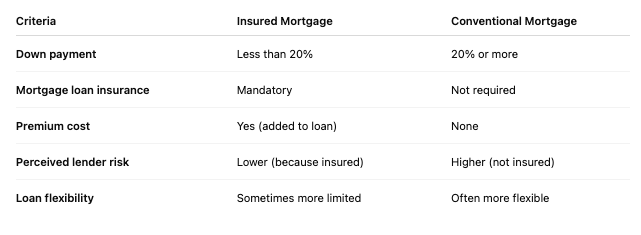

When applying for a mortgage in Canada, one of the most important distinctions to understand is whether your loan will be insured or conventional. If your down payment is less than 20% of the purchase price, mortgage loan insurance is mandatory. If you put down 20% or more, you may qualify for a conventional mortgage, which comes with fewer costs and more flexibility. Understanding the difference can help you make smarter, more cost-effective decisions.

What is an insured mortgage?

An insured mortgage is required when your down payment is less than 20% of the home’s purchase price. In this case, your lender must obtain mortgage loan insurance from a provider such as:

Purpose of the insurance:

This insurance protects the lender — not the buyer — in case of default. In exchange for this safety net, the buyer pays a premium that is added to the mortgage amount.

How much does it cost?

What is a conventional mortgage?

Key advantages:

Comparaison rapide