Life insurance is a cornerstone of financial planning. It provides peace of mind by ensuring that your loved ones are financially protected in the event of premature death. However, as your personal, family, and financial situation evolves over time, your insurance needs may also change. Understanding the types of coverage available — and reviewing them regularly — is key to keeping your protection aligned with your goals.

Why You Should Regularly Review Your Coverage

Life is constantly changing. Marriage, children, homeownership, career shifts, debt, or even divorce — all these events can significantly impact your financial responsibilities and priorities. A coverage amount that was adequate years ago may now be outdated or insufficient.

That’s why it’s essential to review your life insurance coverage periodically. Doing so allows you to:

-

Ensure the amount of coverage still meets your needs

-

Adjust the term length based on new responsibilities

-

Update beneficiaries

-

Optimize your coverage to match your current objectives

A parent with young children may want higher coverage than someone approaching retirement whose children are financially independent.

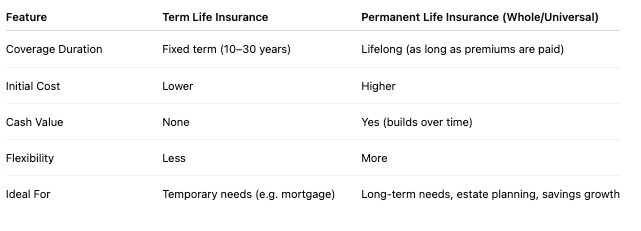

When Does Term Life Insurance Make Sense?

Term life insurance is designed to cover temporary needs. It offers an affordable solution for people with limited budgets or specific time-bound obligations. It’s often the best option when you want to:

-

Protect a mortgage or long-term debt

-

Fund your children’s postsecondary education

-

Secure coverage early in your career when permanent policies are too costly

Term life insurance typically covers a fixed period (10, 20, or 30 years). It has no cash value, making it more affordable than permanent insurance. At the end of the term, the coverage expires unless renewed — often at a higher cost due to age.

Certain permanent life insurance policies — like whole life or universal life — come with a cash value component. This value grows over time and can be accessed by the policyholder in various ways:

-

Borrow against it in times of need

-

Use it to pay future premiums

-

Supplement retirement income

-

Leave a tax-efficient inheritance

It’s a long-term financial tool that goes beyond just death benefit protection.

Most life insurance contracts in Canada include a suicide exclusion clause for the first 24 months after the policy is issued. This provision is intended to:

After this two-year period, the death benefit is generally paid in full, regardless of cause — including suicide. It’s an important clause to be aware of when purchasing a policy.

Your life insurance coverage should evolve with your life circumstances. A trusted advisor will review your needs periodically by evaluating:

- Changes in income

- Family composition

- Debts and assets

- Retirement and estate planning goals

Life insurance isn’t a “set it and forget it” product — it’s a customizable, evolving protection tool. Whether you need term insurance for a temporary obligation or a permanent policy to build long-term value and legacy, choosing the right product at the right time is critical.

Regular reviews ensure that your coverage remains:

- Aligned with your life’s stage

- Adequate for your responsibilities

- Optimized for your evolving goals

By combining tools like the Home Buyers’ Plan (HBP) and the First Home Savings Account (FHSA), a couple could accumulate up to $200,000 tax-free for a down payment — which, in turn, influences insurance needs when taking on a mortgage.