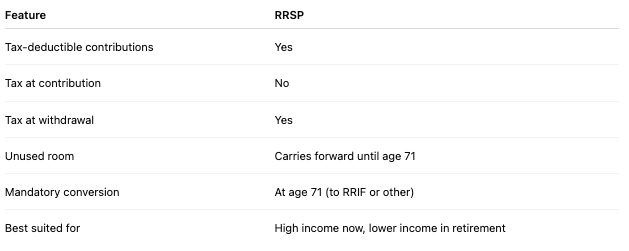

The Registered Retirement Savings Plan (RRSP) is one of Canada’s most important retirement savings tools. It offers valuable tax advantages and flexibility in managing retirement income. However, understanding its rules is essential to make the most of it.

Contribution room carries forward… but not indefinitely

Each year, you accumulate RRSP contribution room, based on a percentage of your earned income from the previous year (up to a maximum set by the Canada Revenue Agency).

-

If you don’t contribute the full allowable amount, your unused contribution room carries forward.

-

You can use it in future years when it may be more advantageous.

If your deduction limit is $5,000 this year and you don’t contribute anything, that $5,000 will be added to your contribution room next year.

At age 71, you must close or convert your RRSP. At that point, any unused contribution room expires.

Mandatory conversion at age 71: Moving to a RRIF

The government imposes an age limit on deferring taxes on RRSP savings:

Empty space, drag to resize

- Close your RRSP

- Or convert it, usually into a RRIF (Registered Retirement Income Fund)

This rule ensures that tax-deferred funds are eventually taxed, rather than sheltered indefinitely.

One of the biggest benefits of the RRSP is that contributions are tax-deductible:

- You pay less tax now

- You pay tax later, likely at a lower rate during retirement, maximizing your net benefit.

RRSPs are especially advantageous for high-income earners, as their marginal tax rates are higher.

-

The higher your marginal rate, the more valuable each dollar of contribution becomes.

-

This also reduces your taxable income, potentially lowering your overall tax burden.

However, if you’re in a lower tax bracket now or expect to earn more later, you might delay contributions or consider alternatives like a TFSA.

The TFSA (Tax-Free Savings Account) doesn’t provide an upfront deduction but allows for tax-free withdrawals. It’s often more suitable for lower-income earners or those who may need to access funds before retirement.

-

Your income is high now

-

You expect a lower income in retirement

-

You want an immediate tax refund

-

You can keep the funds invested until retirement

The RRSP is a powerful tool for tax deferral and retirement savings, but it must be used strategically. Understanding how contribution room accumulates, when to contribute or convert, and how it fits with your tax situation helps you optimize both short-term savings and long-term income. Speak with a financial advisor to integrate RRSPs into a plan that reflects your personal goals and circumstances.